The thesis in one frame: shift the centre of gravity from buying attention to earning a place in the shortlist — across classic search and AI answers — while defending the brand-demand moat the company already paid to build.

Why we pulled this brand apart

Mamaearth is not a startup learning paid media. It is the flagship of India's largest digital-first beauty and personal care company by revenue, sitting inside a parent that deployed Rs 788 crore on advertising in FY26 alone. The interesting question is therefore not whether this brand can run ads, but whether a mature, ad-heavy machine is being pointed at the right surfaces as product discovery itself migrates away from the channels that built it.

This teardown maps that question end to end: the business model, the funnel, the Google and Meta engines, the keyword universe, the competitive set, the creative and CRO systems, a budget framework, and the discovery shift toward AI answer engines that will decide the next five years of beauty marketing in India. It is the same lens we bring to a paid-media engagement or an answer-engine-optimization programme for our own clients.

It is built entirely from public sources: company filings and earnings commentary, named industry and market data, observable advertising and landing-page behaviour, and structured strategic reasoning. Hard figures are cited where the company discloses them; where Mamaearth does not break out a number publicly, the analysis works with directional estimates and benchmark ranges and says so in plain language rather than presenting a guess as a fact. Nothing here relies on internal or proprietary data, and the full disclaimer at the end states this explicitly. The study is written so that any operator in this category, including a direct competitor, could read it and act on it.

One scope note before we begin. The Derma Co and Aqualogica are routinely grouped with Mamaearth's rivals. They are not competitors at all. Both are sister brands inside the same parent, Honasa Consumer, alongside BBlunt, Dr. Sheth's, Staze, Ayuga, the Nykaa-exclusive prestige line Lumineve, the acquired men's grooming brand Reginald, and the oral-care stake Fang Oral. This distinction reshapes the competitive and conquest sections below, so it is surfaced here at the top rather than buried.

Headline numbers at a glance

| Metric | Figure | Why it matters |

|---|---|---|

| FY26 operating revenue (Honasa) | Rs 2,392 crore | Up roughly 16 to 20 percent year on year after a slow FY25 |

| FY26 profit after tax | Rs 200 crore | Nearly tripled from Rs 72.6 crore, first-ever dividend declared |

| FY26 advertising spend | Rs 788 crore | About 33 percent of revenue, the single largest controllable cost line |

| Ad intensity vs peers | ~33 percent vs 40 to 50 percent norm | Lower than the typical D2C beauty challenger, and falling |

| Revenue growth trajectory | 28.6 percent (FY24), ~8 percent (FY25), ~20 percent (FY26) | The dip and recovery that frames the whole strategy |

| The Derma Co ARR | Above Rs 750 crore | Sister brand, not a competitor, and a second engine |

| AI product-discovery share | ~37 percent of queries start in AI tools | The shift this study is built around |

| AI-referred conversion rate | ~12.3 percent vs 3.1 percent non-AI | Why answer-engine visibility is worth fighting for |

The position, read honestly

Before the plays, the snapshot. Where is this brand actually strong, and where is it exposed?

| Dimension | Assessment |

|---|---|

| Brand strength | Very high. Top-of-mind in toxin-free and ingredient-led personal care, with founder-led equity (Varun and Ghazal Alagh, the latter a Shark Tank India judge) |

| Market positioning | Mass-premium (Rs 200 to 500 band). Strong, but structurally the slower-growth tier of the market |

| Search visibility (organic) | Strong on branded terms, thinner on non-brand category and concern terms |

| Paid visibility | Extensive and well-funded across Google and Meta. The surface mix is the open question |

| Funnel maturity | High at the top (awareness) and mid (consideration). Retention and subscription look underdeveloped relative to spend |

| AI-search readiness | The single biggest unguarded flank. Ingredient-led discovery is exactly what answer engines are absorbing |

Five findings frame everything that follows.

First, Mamaearth is advertising-intensive, but less so than its peers. Honasa's FY26 ad spend of Rs 788 crore is roughly 33 percent of reported revenue (Rs 2,392 crore). That is a large number, but the wider D2C beauty norm runs 40 to 50 percent of revenue. The real story of FY25 into FY26 is a deliberate move away from raw performance spend toward brand-building and media-mix discipline.

Second, the growth deceleration of FY25 was a paid-acquisition warning shot. Revenue growth fell from roughly 28.6 percent in FY24 to about 8 percent in FY25 before recovering to roughly 20 percent in FY26. The recovery came from category focus, media-mix modelling, and awareness-led building, not from simply spending more. This is the clearest public signal that the cheap-paid-acquisition era has ended for the brand.

Third, the portfolio, not the single brand, is the real competitive unit. The Derma Co has crossed an annual revenue run rate above Rs 750 crore and is Euromonitor's number one sunscreen brand in India. Treating it as a conquest target would be self-cannibalisation.

Fourth, discovery is migrating to AI answer engines, and beauty is the front line. Roughly 37 percent of product-discovery queries now start in AI interfaces, and AI-referred shoppers convert at around 12.3 percent versus 3.1 percent for non-AI traffic. For an ingredient-led brand, this is both the largest risk and the largest unclaimed opportunity.

Fifth, the biggest opportunities and risks both cluster around the same shift. The opportunities: own the non-brand ingredient and concern universe before answer engines settle their citation patterns; convert review and editorial density into AI citations; tilt the paid mix toward retail media and quick commerce; and build retention and subscription economics. The risks: disintermediation by AI Overviews and chat assistants on exactly the queries Mamaearth's hero products are built to answer; well-capitalised strategic owners now controlling the fastest-growing rivals; and a tier mismatch, with the core sitting in the slower-growing mass-premium band while the 18 percent CAGR action is one tier up.

The strategic recommendation in one line: shift the marketing centre of gravity from buying attention on Meta and Google to earning inclusion in the shortlist, across both classic search results and AI answers, while protecting the brand-demand moat the company has already paid to build.

How the money actually works

Mamaearth sits inside a House of Brands, so the money has to be read at both the brand and the parent level.

| Layer | FY26 figure |

|---|---|

| Honasa operating revenue (reported) | Rs 2,392 crore, up roughly 16 to 20 percent year on year |

| Honasa profit after tax | Rs 200 crore, up from Rs 72.6 crore in FY25 |

| Honasa FY26 advertising spend | Rs 788 crore |

| Full-year EBITDA margin | About 9.3 percent, with Q4 reaching 11.3 percent |

| First-ever dividend | Rs 3 per share, roughly Rs 98 crore payout |

The Mamaearth brand returned to double-digit growth in FY26 and re-took share in face cleansers, entering the top five in face wash. The parent does not break out brand-level revenue publicly, so this study works with the disclosed portfolio numbers and treats brand-level splits as directional.

The table below reads category-level value across the personal-care portfolio. Mamaearth does not disclose category splits, so the ranking is a directional read drawn from product salience, public commentary on hero SKUs, repeat-purchase logic, and category economics.

| Category | Role in the brand | Repeat-purchase intensity | Margin character | Strategic value |

|---|---|---|---|---|

| Face wash / cleansers | Hero volume engine. Ubtan and Rice face wash are named growth drivers, with Rice Face Wash alone reaching a Rs 100 crore ARR run rate | High (frequent replenishment) | Mid to high | Highest. Entry product and a category Mamaearth now leads |

| Hair care (shampoo, oil) | Second engine. Onion Shampoo and Rosemary Anti-Hair-Fall Shampoo are named performers | High | Mid | Very high. Hair fall is a durable, high-intent concern |

| Serums / actives (Vitamin C) | Bridge into premium routines | Medium to high | High | High. Higher AOV, ladders into the faster-growing tier |

| Sunscreen | Growing, though the parent's sunscreen crown sits with The Derma Co | Medium (seasonal skew) | High | Medium for Mamaearth specifically |

| Moisturiser | Routine staple, cross-sell anchor | High | Mid | Medium to high |

| Baby care | The founding category and trust origin story | Very high (lifecycle loyalty) | Mid | High for LTV and brand meaning, smaller for absolute scale today |

| Body care / conditioner | Basket builders | Medium | Mid | Medium (attach-rate plays) |

The most valuable categories combine high purchase frequency with defensible search intent: face wash and hair care. The highest-LTV category is arguably baby care, because it captures a household early and retains across a parenting lifecycle. The highest-margin categories are serums and sunscreen, which also happen to be where the premium tier and AI-driven ingredient discovery concentrate. The implication is that paid budget should over-index on hair care and face wash for efficient volume, while content and AI-visibility investment should over-index on serums, actives, and concern-led skincare to defend future margin. This is precisely the split a D2C growth programme has to get right.

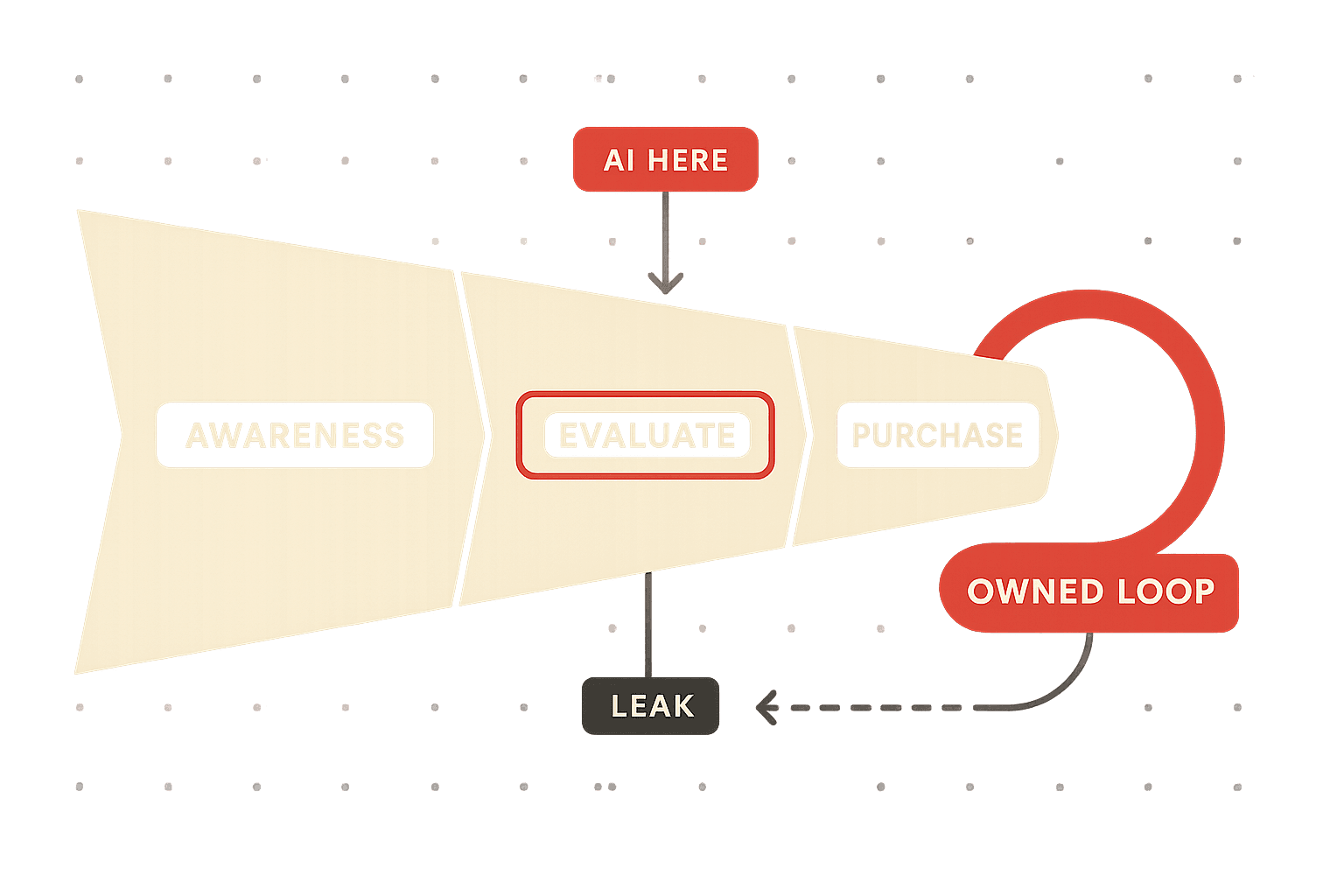

The journey a buyer actually takes

The funnel below is built for an ingredient-led, mass-premium beauty brand selling across owned D2C, marketplaces, and quick commerce. The missed-opportunity column is where most of the upside lives.

The two cheapest sources of incremental revenue for a brand this mature are not at the top of the funnel — they are the consideration-to-evaluation band where AI answers now adjudicate, and the retention loop where owned channels can replace paid re-acquisition.

| Stage | Dominant user intent | Where it happens now | PPC and discovery opportunity | Common missed opportunity |

|---|---|---|---|---|

| Awareness | "My hair is falling, what helps" or "is this ingredient safe" | Instagram, YouTube, AI chat, Google | Demand-gen on Meta and YouTube, broad concern keywords, AI-citation content | Treating awareness as a Meta-only game while AI answers quietly pre-decide the shortlist |

| Consideration | "Best onion shampoo for hair fall" or "X vs Y" | Google, marketplaces, review sites, Reddit, AI chat | Non-brand category and comparison search, Shopping, review density | Under-owning comparison and "best" queries that map directly to AI answer prompts |

| Evaluation | "Mamaearth onion shampoo review" or "does it work" | Reviews, YouTube, marketplace ratings | Branded defensive search, review acquisition, PDP CRO | Weak structured proof (clinical, dermatologist, schema) that both humans and LLMs read |

| Purchase | Buy intent, often on a marketplace or quick-comm app | Amazon, Flipkart, Nykaa, Blinkit, Zepto, own site | Retail media (Amazon Ads, Flipkart, quick-comm networks), brand search defence, Shopping | Over-indexing Google or Meta while the transaction migrates to retail media |

| Retention | Replenishment, routine completion | Email, WhatsApp, subscription, app | Dynamic remarketing, subscription, cross-sell, win-back | Re-buying the same customer through cold paid instead of owned retention |

The structural insight is that for a brand of this maturity, the cheapest incremental revenue is no longer at the top of the funnel. It sits in two places this study keeps returning to: the consideration-to-evaluation band where AI answers now adjudicate, and the retention loop where owned channels can replace paid re-acquisition. A great deal of paid budget in mature D2C beauty is spent re-winning customers the brand already owns, which depresses blended return on ad spend without anyone in a single campaign seeing it.

The paid-search engine, reverse-engineered

This is a structural read of how a brand with Mamaearth's footprint runs search, reconstructed from observable ad behaviour, landing-page architecture, ad-copy patterns, the known hero SKUs, and category norms. The value is in the architecture and the gaps, both of which any operator can pressure-test against their own account.

| Campaign type | Present | What it should be doing |

|---|---|---|

| Brand | Yes | Defending "mamaearth", "mamaearth face wash", "mamaearth onion shampoo" at near-total impression share. These are the brand's top organic and paid terms, which means they are also the most contested by resellers and marketplaces |

| Generic / category | Partially | Capturing "onion shampoo", "vitamin c face wash", "ubtan face wash", "hair fall shampoo" as a non-brand acquisition engine |

| Competitor / conquest | Uncertain | Bidding on external rivals only, with the critical sister-brand caveat below |

| Concern / problem-aware | Likely thin | "how to reduce hair fall", "best face wash for oily skin" map to high-volume, high-AI-overlap demand |

What looks strong: brand-demand capture (years of brand investment mean enormous branded query volume to harvest cheaply), hero-SKU specificity (named products like Onion, Ubtan, Rice and Vitamin C give clean, high-intent keyword-to-landing-page matches), and offer cadence (frequent promotions suit Shopping and brand search).

What looks weak: non-brand category depth (if branded terms dominate the keyword profile, the brand is paying to capture demand it already created rather than expanding it) and concern-led intent (problem-aware queries like "hair fall treatment" and "acne face wash" are where new customers form preferences, and where AI answers are most active).

What looks missing: a deliberate answer-engine layer. Classic Google Ads does not address the share of "best X for Y" queries now resolved inside AI Overviews and chat, which sit above the paid auction entirely.

Four practical plays follow from that read. Lock brand impression share and run an ongoing reseller and sister-brand overlap check so the portfolio is not bidding against itself. Expand a non-brand category cell structured by ingredient plus concern plus form, mirrored exactly to PDP and content. Re-cut ad copy around proof, not adjectives — dermatologist-tested, clinically observed, specific concentrations — copy that doubles as AI-citation fodder. And use Performance Max as a feed-led engine, not a black box, with hero SKUs ring-fenced into their own asset groups — the discipline at the heart of any serious Google Ads programme.

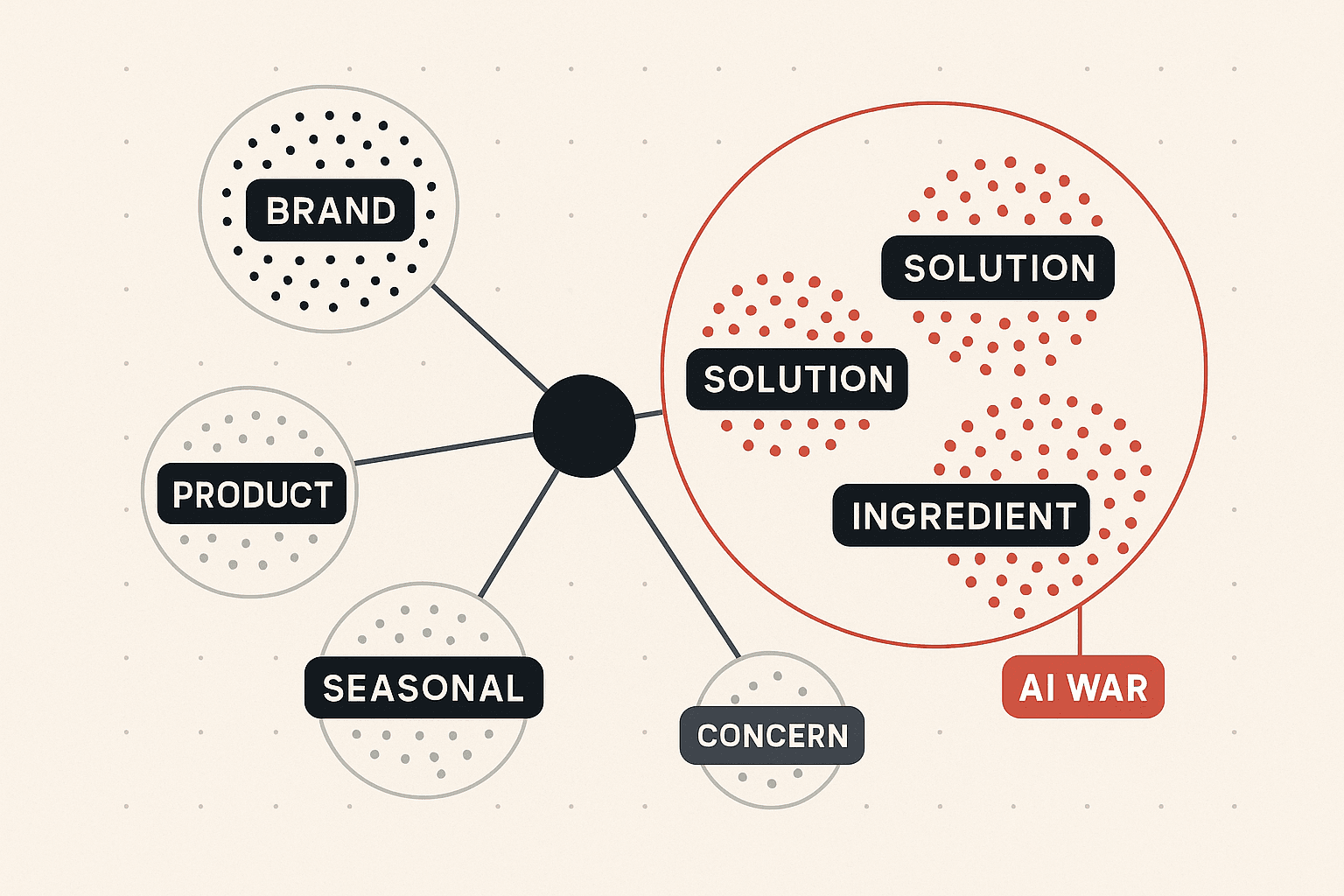

The keyword universe. This is a keyword architecture rather than a volume dump. What drives allocation is not the raw number next to each term but its intent, funnel stage, commercial value, and priority. Volume bands are relative, not measured absolutes.

Paid efficiency is best protected on brand and product clusters — but future growth and the AI-search defence live in the solution-aware, ingredient-based and concern-based clusters, where the language of a paid query and the language of a ChatGPT prompt are now identical.

Brand cluster

| Example terms | Intent | Funnel stage | Commercial value | PPC priority |

|---|---|---|---|---|

| mamaearth, mamaearth face wash, mamaearth onion shampoo, mamaearth products | Navigational / transactional | Evaluation to Purchase | Very high (highest conversion rate) | Defend at all costs |

Product cluster

| Example terms | Intent | Funnel stage | Commercial value | PPC priority |

|---|---|---|---|---|

| onion shampoo, ubtan face wash, rice face wash, vitamin c serum, rosemary hair oil | Transactional | Consideration to Purchase | High | High |

Problem-aware cluster

| Example terms | Intent | Funnel stage | Commercial value | PPC priority |

|---|---|---|---|---|

| hair fall treatment, how to reduce hair fall, why is my skin oily, dark spots on face | Informational to commercial | Awareness to Consideration | Medium to high (preference forms here) | High for content and AI, medium for paid |

Solution-aware cluster

| Example terms | Intent | Funnel stage | Commercial value | PPC priority |

|---|---|---|---|---|

| best shampoo for hair fall, best face wash for oily skin, niacinamide vs vitamin c | Commercial investigation | Consideration | High | High (the AI-answer battleground) |

Competitor cluster (external only)

| Example terms | Intent | Funnel stage | Commercial value | PPC priority |

|---|---|---|---|---|

| minimalist alternative, plum vs mamaearth, cetaphil dupe | Comparative | Consideration | Medium to high | Medium (handle with care, see the conquest section) |

Ingredient-based cluster

| Example terms | Intent | Funnel stage | Commercial value | PPC priority |

|---|---|---|---|---|

| niacinamide serum, salicylic acid face wash, hyaluronic acid moisturiser, spf 50 sunscreen | Informational to transactional | Consideration to Purchase | High | Very high (ingredient queries are AI-native) |

Concern-based cluster

| Example terms | Intent | Funnel stage | Commercial value | PPC priority |

|---|---|---|---|---|

| acne face wash, anti ageing serum, sun tan removal, dandruff shampoo | Commercial | Consideration to Purchase | High | High |

Seasonal cluster

| Example terms | Intent | Funnel stage | Commercial value | PPC priority |

|---|---|---|---|---|

| summer sunscreen, winter dry skin cream, festive gift sets, monsoon hair care | Transactional, time-boxed | Consideration to Purchase | Medium to high in-season | Burst budgeting around peaks |

The one keyword principle that matters most: paid efficiency is best protected on brand and product clusters, but future growth and the AI-search defence live in the solution-aware, ingredient-based, and concern-based clusters. Those three are where the language of a paid query and the language of a ChatGPT prompt are now identical. Winning them in content and reviews is what gets a brand named when the auction disappears.

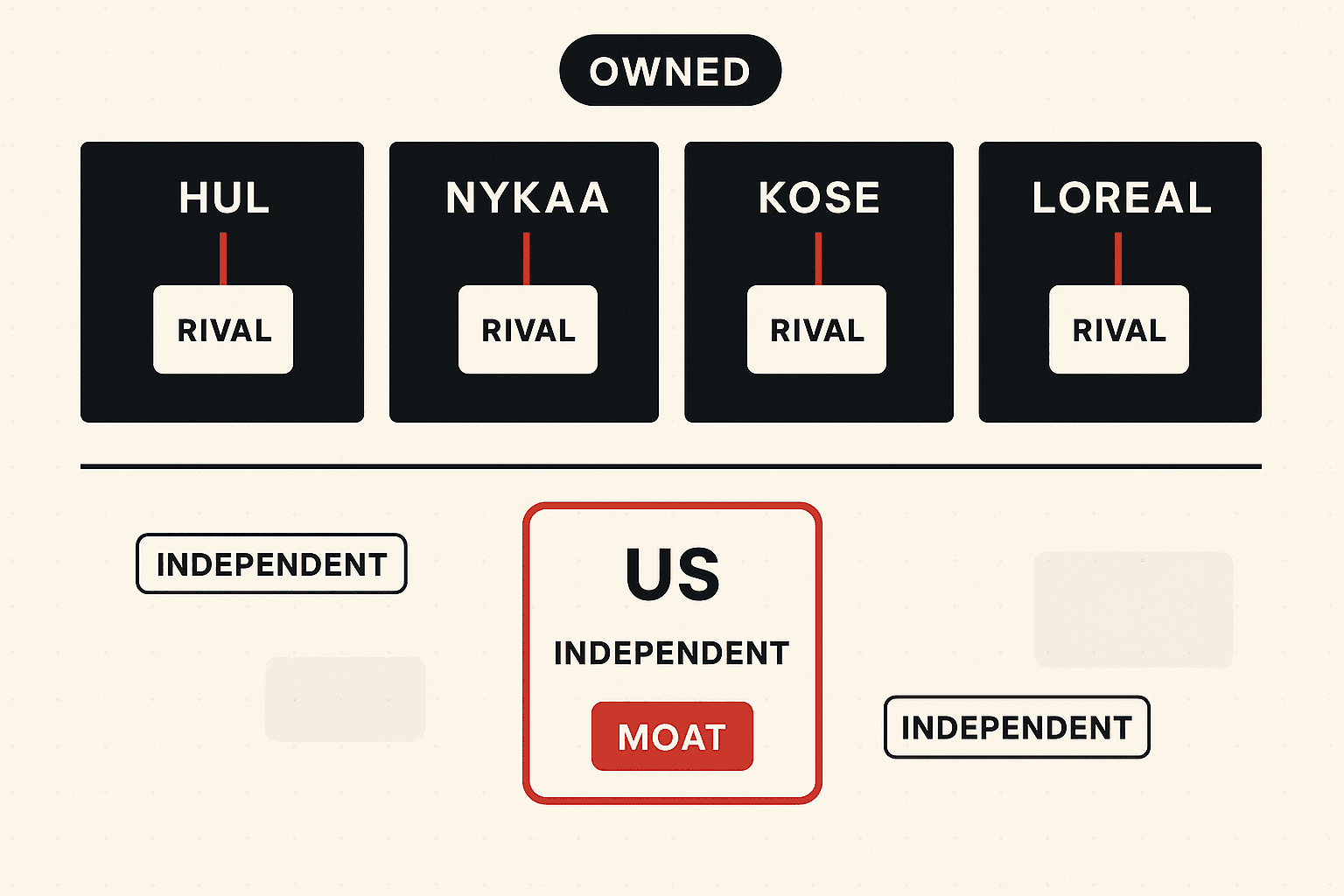

The competitor question everyone gets wrong

The Derma Co and Aqualogica are often listed as Mamaearth's rivals. They are sister brands inside Honasa Consumer, alongside BBlunt, Dr. Sheth's, Staze, Ayuga, the Nykaa-exclusive prestige line Lumineve, the acquired men's grooming brand Reginald, and the oral-care stake Fang Oral. Running competitor-conquest paid activity against any of these means paying to take clicks from the same parent. The portfolio is the moat, not the target. The genuine external set is narrower and, importantly, increasingly owned by strategic giants.

The fastest-growing rivals are being rolled up by HUL, Nykaa, KOSE and L'Oreal. Mamaearth and Honasa now sit among the few scaled independents left standing — a vulnerability and a positioning asset at once.

| External competitor | Positioning | Ownership / backing | Why it matters now |

|---|---|---|---|

| Minimalist | Science-first, ingredient transparency, restraint in marketing | HUL (90.5 percent, about Rs 2,706 crore, 2025) | Now has FMCG distribution muscle and patient capital behind a brand already trusted in actives |

| Dot and Key | Routine-led, vibrant, fast-moving skincare | Nykaa (majority, August 2024) | Owned by the platform that also controls discovery and shelf on Nykaa |

| Foxtale | Modern actives skincare | KOSE Corporation (strategic) | Global formulation and capital backing |

| Plum | Vegan, clean, accessible | VC-backed, independent | Strong own-site and routine bundling |

| Pilgrim | Global-inspired formulations | VC-backed, about Rs 3,000 crore valuation (2025) | Aggressive launch cadence |

| WOW Skin Science | Natural, ACV haircare heritage | Independent, has explored a sale at a reduced valuation | A weakening rival, a clear conquest opportunity |

| Cetaphil / CeraVe | Dermatologist-recommended global derma-cosmetics | Galderma / L'Oreal | Own the "dermatologist says" trust ladder, including inside AI answers |

| Biotique | Ayurvedic mass-premium | Independent | Overlaps the natural positioning directly |

The pattern is unmistakable. The fastest-growing rivals are being rolled up by HUL, Nykaa, KOSE, L'Oreal, and others. Mamaearth and Honasa now sit among the few scaled independents left standing, which is simultaneously a vulnerability (deep-pocketed owners) and a positioning asset (the credible founder-led independent).

Opportunity score below weighs how winnable share is through paid conquest plus content. Difficulty weighs the rival's defensive strength. Scores run 1 to 10.

| Competitor | Opportunity score | Difficulty | Priority | Rationale |

|---|---|---|---|---|

| WOW Skin Science | 8 | 3 | 1 | Weakening, overlapping natural positioning, vulnerable on share |

| Biotique | 7 | 4 | 2 | Adjacent natural positioning, beatable on ingredient proof |

| Pilgrim | 6 | 5 | 3 | Beatable on trust and scale, but launch-heavy and noisy |

| Plum | 6 | 6 | 4 | Strong own-site loyalty, contest on price-value |

| Dot and Key | 5 | 7 | 5 | Nykaa-owned, well defended on its home platform |

| Foxtale | 5 | 7 | 5 | Well-funded and modern, hard to dislodge |

| Minimalist | 4 | 8 | 6 | HUL-backed, conquest is expensive, contest on accessibility instead |

| Cetaphil / CeraVe | 4 | 9 | 7 | Do not fight on dermatologist, flank on natural-plus-efficacy |

The conquest plays follow directly. Prioritise the weak and the overlapping (WOW, Biotique) for direct conquest search and comparison content. Flank, do not charge, the strong (Minimalist, CeraVe) — win "natural and clinically tested" rather than out-spending on "dermatologist". Treat comparison content as dual-purpose: a "Mamaearth vs X" page is both a conquest landing page and an AI-citation asset for "X alternative" prompts — exactly the kind of asset a content marketing programme is built to produce at scale. And never run conquest against the House of Brands — build a negative-keyword and exclusion governance layer across the portfolio's accounts.

The channel audits: Shopping, PMax, Meta and retention

Google Shopping and Performance Max. Shopping is where ingredient-and-concern intent converts, and where feed quality silently decides who wins.

| Lever | What good looks like | The gap most catalogues leave |

|---|---|---|

| Product titles | Brand plus product plus key ingredient plus concern plus form plus size, front-loaded | Titles that lead with brand and product name and under-use ingredient and concern keywords |

| Product types / categories | Granular taxonomy matching how shoppers search | Broad categories that miss concern-level grouping |

| Attributes | Complete GTIN, size, count, highlights, skin type | Variable completeness across a large catalogue |

| Imagery | Clean primary plus ingredient and benefit lifestyle shots | Usually strong for this brand category |

| Pricing and promotions | Sale price and promotion annotations live | Underused promotion markup |

The Shopping plays: re-title hero SKUs around the search query, not the shelf ("Mamaearth Vitamin C Face Wash for Oily Skin, with Vitamin C and Turmeric, 100ml" beats "Mamaearth Vitamin C Face Wash"); add concern-level product types (anti-hair-fall, oily-skin, dark-spots) so the feed can map to concern queries; fill every optional attribute, especially skin type and product highlights, because these increasingly feed both Shopping and AI shopping surfaces; and use Merchant Center promotions and ratings aggressively, since star ratings carry into how products are perceived and cited.

For a mature ecommerce advertiser, Performance Max is almost certainly running. The risk at this scale is that PMax becomes an unaccountable spend sink that quietly harvests brand demand and reports it as prospecting.

| PMax element | What good looks like | The gap to watch |

|---|---|---|

| Asset groups | Themed by category and concern, hero SKUs ring-fenced | One giant catch-all group |

| Audience signals | First-party lists, cart and purchaser seeds, concern-based intent | Under-segmented signals |

| Creative diversity | Multiple ratios, UGC, proof-led statics and video | Often the weakest input at scale |

| Feed strategy | Feed-led PMax with strong titles | Dependent on Merchant Center quality |

| Landing-page alignment | Concern-specific PDPs and collection pages | Generic category pages |

| Brand traffic control | Brand excluded or measured separately | The classic leak: brand demand counted as PMax wins |

The recommended PMax architecture: separate brand from non-brand (use brand exclusions so PMax is measured on incremental, not harvested, demand); build concern-themed asset groups (hair fall, oily skin, sun protection, baby care), each pointed at a matching PDP or collection; feed every asset group proof-led creative (before-and-after where compliant, ingredient call-outs, dermatologist framing, review quotes); ring-fence hero SKUs into dedicated asset groups so winners are not diluted by the long tail; and instrument a clean conversion-value model so true incremental ROAS is visible to both marketing and finance.

Meta, creative and CRO. Meta remains the demand-generation engine for D2C beauty, but the economics have shifted: CPMs have risen, signal loss from privacy changes has degraded targeting, and the same audiences are contested by hundreds of brands. The category runs a recognisable repertoire of creative and offer patterns — founder and purpose storytelling, ingredient-led hooks (onion, ubtan, vitamin C, rice), before-and-after result framing, dermatologist endorsement, UGC-style testimonial video, problem-agitate-solve hooks, bundle and combo offers, festive promotions, free-gift mechanics, social-proof statics, "Made Safe" trust badges, creator collaborations, concern-specific carousels, routine education, myth-busting, seasonal angles, price-anchored value, app and subscription nudges, marketplace-availability cues, and quick-commerce immediacy.

Where do competitors do it better? Minimalist leans into restraint and clinical credibility, which reads as trust rather than noise — and in an AI-citation world, that clinical content compounds. Dot and Key runs vibrant, routine-led creative that bundles multiple SKUs into a single basket, lifting units per order. Foxtale and Pilgrim push high creative velocity, testing more hooks per week.

The plays here are about leverage, not budget. Increase creative velocity and proof density, not spend — at this maturity the constraint is winning creative, not reach. Build a UGC and creator engine whose outputs double as review and AI-citation material. And shift a measured share of Meta budget toward retail media and quick commerce, where purchase intent now concentrates — the same migration we map for ecommerce brands as the transaction moves off owned D2C.

The landing-page picture, scored 1 to 10 where 10 is best in class, reflects category norms and the brand's known assets:

| Area | Homepage | Category pages | Product pages | Score | Priority |

|---|---|---|---|---|---|

| Trust signals | Strong (certifications, founder story) | Medium | Strong | 8 | Maintain |

| Social proof / reviews | Medium | Medium | Strong on hero SKUs, thin on long tail | 6 | High |

| Guarantees | Variable | Variable | Variable | 5 | Medium |

| Bundles and routines | Underused | Underused | Some | 5 | High |

| Upsell / cross-sell | Light | Light | Some | 5 | High |

| Mobile UX | Strong (roughly 90 percent of traffic is mobile) | Strong | Strong | 8 | Maintain |

| Page speed | Medium | Medium | Medium | 6 | Medium |

| Conversion friction (checkout) | Medium | n/a | Medium | 6 | Medium |

| Machine-readability (schema) | Partial | Partial | Partial | 4 | Highest (AI-search) |

The CRO finding that matters most: for a brand this far along, the highest-return work is not another hero-banner test. It is two things. First, structured proof on PDPs (reviews, clinical or dermatologist framing, FAQ schema, ingredient detail) that lifts human conversion and makes pages retrievable by answer engines — the machine-readability layer a technical SEO programme owns. Second, routine and bundle architecture that raises units per order, because in a rising-CPM world the cheapest way to improve blended economics is to sell more per checkout rather than win more checkouts.

The retention loop most brands underbuild. A mature advertiser's remarketing should be a layered audience architecture, not a single "all visitors" pool.

| Layer | Audience definition | Message | Priority |

|---|---|---|---|

| Dynamic remarketing | Viewed-but-not-bought, by product | The exact product plus proof plus light incentive | High |

| Cart abandonment | Added to cart, no purchase, 0 to 7 days | Urgency plus free-shipping or gift threshold | Highest (cheapest recovery) |

| Product-view retargeting | Browsed a concern category | Routine education plus the matching hero SKU | High |

| Cross-sell | Bought face wash | Matching moisturiser or serum to complete routine | High |

| Upsell | Bought single SKU | Bundle or larger size at value framing | Medium |

| Subscription | Repeat buyers of consumables | Subscribe-and-save on shampoo, face wash | High (LTV lever) |

| Repeat purchase / replenishment | Past buyers near replenishment date | Timed reminder plus reorder ease | High |

| Win-back | Lapsed 90 to 180 days | We-miss-you plus what is new | Medium |

The remarketing thesis: the biggest unglamorous win for a brand spending at this level is to move replenishment and routine-completion off cold paid and onto owned channels (email, WhatsApp, app, subscription). Every customer retained through owned media is a customer who does not need to be re-bought at a rising CPM. This is the clearest path to lifting blended return on ad spend without cutting growth.

YouTube, which now pays twice. YouTube matters twice over. It is a major awareness and consideration surface in India, and it is the single largest citation source inside Google AI Overviews. Winning YouTube now pays a discovery dividend and an AI-visibility dividend at the same time.

| Campaign tier | Objective | Format | Creative concept | Audience | KPI |

|---|---|---|---|---|---|

| Awareness | Reach and brand lift | Bumpers, in-stream | Founder and purpose, ingredient origin | Broad beauty and parenting interest | Views, lift, CPM |

| Consideration | Concern education | In-stream, in-feed | "Why your hair is falling and what helps" | Concern-based intent | View-through rate, site visits |

| Product | Action | In-feed, Shorts | Demo, before-and-after, routine | In-market beauty, remarketing | Conversions, ROAS |

The scripts should be written so the transcript itself becomes AI-citation material, since answer engines read YouTube transcripts heavily. A concern-led hook ("If your hair is falling more than usual, it is probably one of these three things") names the causes, positions the onion or rosemary range as the fix, and closes with proof and offer. An ingredient hook ("Dermatologists keep saying this about vitamin C, and most face washes get it wrong") explains the ingredient, shows the formulation, and closes with the hero SKU. A Shorts hook is a five-second visible result moment, then the product, then where to buy, including quick commerce.

On creative more broadly, fifty angles ranked by a blend of likely performance and AI-citation value cluster into three bands. The deploy-now (A) band is built around ingredient proof, before-and-after results, dermatologist explainers, concern solves (hair fall, oily skin), routine completion, "toxin-free / Made Safe" trust, real customer UGC, myth-busting, "best for [concern]" comparison, subscription value, bundles, sensitive-skin reassurance, sun-protection education, and baby-care lifecycle trust. The test (B) band covers ingredient origin, clinical framing, creator co-signs, seasonal angles, quick-commerce immediacy, price-value anchors, founder-led purpose, switch messaging, ingredient-vs-ingredient education, skin-type quizzes, awards, sustainability, festive gifting, men's crossover, concern bundles, sensory demos, regional-language creative, and first-purchase incentives. The situational (C) band holds loyalty, behind-the-formulation, community, cause tie-ins, limited drops, collaborations, trend-jacking, humour, day-in-the-life, unboxing, dupe framing, nostalgia, long-form expert interviews, data reveals, and shoppable streams. The principle: over-index the A band, which clusters around ingredient proof, concern-solving, and structured credibility — the angles that perform in paid and get cited in AI answers. Adjective-led brand fluff does neither.

The budget question

The one verified channel-level figure is the parent's total of Rs 788 crore in FY26 across the whole portfolio, roughly Rs 65 crore per month for all brands combined. The models below are recommended allocation frameworks for a single Mamaearth-scale brand programme, built on the 2026 D2C benchmark mix (Meta 40 to 50 percent, Google 25 to 30 percent split across Shopping, brand search, and Performance Max, 15 to 25 percent emerging channels, 5 to 10 percent testing), then adapted for a mature brand with heavy existing brand equity. The adaptation pulls budget toward Shopping, retail media, retention, and AI-search readiness, and away from raw top-funnel Meta.

As budget scales, the mature-brand version tilts steadily toward Shopping and PMax, retail media, retention and AI-search, and away from pure top-funnel Meta. A brand that already paid to create demand should spend proportionally more on capturing and retaining it.

Model A — Rs 10 lakh per month (focused single-category or pilot)

| Channel | Allocation | Rationale |

|---|---|---|

| Meta (prospecting plus retargeting) | 38 percent | Demand gen, but disciplined |

| Google Search (brand plus non-brand) | 18 percent | Defend brand, harvest category |

| Google Shopping plus PMax | 18 percent | Highest-intent conversion |

| Retail media (Amazon, Flipkart, quick-comm) | 12 percent | Capture purchase where it happens |

| Remarketing and retention | 6 percent | Cheap recovery |

| YouTube | 4 percent | Awareness plus AI-citation dividend |

| AI-search readiness and content | 4 percent | The new front, small but non-zero |

Model B — Rs 50 lakh per month (scaled single-brand)

| Channel | Allocation | Rationale |

|---|---|---|

| Meta | 35 percent | Scaled demand gen with a strong creative engine |

| Google Search | 16 percent | Brand defence plus expanded non-brand |

| Shopping plus PMax | 18 percent | Feed-led, brand-excluded PMax |

| Retail media and quick commerce | 14 percent | Growing share as purchase migrates |

| Remarketing and retention | 7 percent | Subscription and replenishment push |

| YouTube | 5 percent | Concern education at scale |

| AI-search, content, digital PR | 5 percent | Build citation density |

Model C — Rs 1 crore per month (mature, full-funnel)

| Channel | Allocation | Rationale |

|---|---|---|

| Meta | 32 percent | Demand gen plus creative testing at volume |

| Google Search | 15 percent | Full brand and category coverage |

| Shopping plus PMax | 18 percent | Hero-SKU ring-fenced, incremental-measured |

| Retail media and quick commerce | 15 percent | Material share, this is where growth converts |

| Remarketing and retention | 8 percent | Owned-channel migration of replenishment |

| YouTube | 6 percent | Awareness plus AI-citation engine |

| AI-search, content hubs, digital PR | 6 percent | Defend and capture answer-engine visibility |

The allocation philosophy: as budget scales, the mature-brand version tilts steadily toward Shopping and PMax, retail media, retention, and AI-search, and away from pure top-funnel Meta. The logic is simple. A brand that has already paid to create demand should spend proportionally more on capturing and retaining it, and proportionally less on re-announcing itself to cold audiences at rising CPMs.

The shift that decides the next five years

This is the most consequential part of the teardown, and the one most likely to separate the brands that compound from the brands that quietly fade. Beauty and skincare are the front line of the discovery shift, because the questions buyers ask ("best vitamin C face wash for oily skin under 400") are exactly the questions answer engines are built to resolve. (If the terminology here is unfamiliar, our primer on SEO vs AEO vs GEO lays out the three layers.)

Old world: a sprawling feed and a list of ten links. New world: a single AI answer that compresses the choice set to roughly five products. Brands now compete for inclusion in a shortlist, not for attention in a feed.

The shift, in numbers: roughly 37 percent of product-discovery queries now begin in AI interfaces like ChatGPT and Perplexity. AI-referred shoppers convert at about 12.3 percent versus 3.1 percent for non-AI traffic, and spend meaningfully longer on site, because the AI has already done the comparison work. ChatGPT operates at very large scale, on the order of 900 million weekly users and roughly 2 billion queries a day, making it a discovery surface in its own right. When a shopper asks an AI for a skincare pick by sensation, concern, and price, the selection set compresses to roughly five products. And the most-cited sources inside Google AI Overviews are YouTube (about 23 percent), Wikipedia (about 18 percent), and Google.com (about 16 percent), while ChatGPT leans heavily on Reddit, major publications, and review platforms.

Each engine shapes beauty discovery a little differently.

| Engine | Behaviour for beauty queries | What gets a brand named |

|---|---|---|

| Google AI Overviews | Summarises "best X for Y" above the links | YouTube presence, Wikipedia or entity strength, review-rich pages, schema |

| ChatGPT | Returns a compressed shortlist with reasons | Reddit sentiment, editorial coverage, marketplace reviews, clear PDPs |

| Gemini | Routine and comparison synthesis, Google-data-rich | The Overviews signals plus structured product data |

| Perplexity | Citation-first answers, fast to update | Fresh, well-sourced editorial and review content, citations land here first |

The tactical playbooks differ by engine — we break them down in how to rank on ChatGPT and how to rank on Perplexity. | Copilot | Shopping-leaning, commerce-data-aware | Structured product data, ratings, retailer presence | | Claude | Reasoned, safety-aware recommendations | Clear evidence, credible authorship, consistent brand facts |

Where Mamaearth risks losing visibility: on solution-aware and ingredient queries ("best onion shampoo for hair fall", "vitamin C vs niacinamide", "best face wash for oily skin") that are AI-native, where thin review or editorial density hands the citation to a rival; on "dermatologist-recommended" framings, where CeraVe and Cetaphil hold a structural head start; and on comparison and "alternative" prompts, where whoever owns the comparison content owns the answer.

Where it can gain visibility: on natural-plus-clinically-tested positioning, a space neither the pure-clinical brands nor the pure-natural brands fully own; on hero-ingredient authority (onion, ubtan, rice, vitamin C), where the brand already has product-market fit and search demand to convert into citation authority; and on lifecycle and baby-care trust, a durable, emotionally weighted entity that AI engines can attach to the brand.

The AEO and GEO action plan has seven moves. Entity SEO and knowledge-graph development — make the brand and its hero products unambiguous machine-readable entities, because AI engines recommend what they can confidently identify. Ingredient content hubs — deep, evidence-led pages on each hero ingredient and concern, written to answer the exact prompts buyers type into AI; these are the highest-leverage assets in the entire plan. Comparison and experience content — honest "X vs Y" and "best for [concern]" pages that earn the comparison-prompt citations. Review acquisition at scale, concentrated on the surfaces AI cites most: marketplace reviews, YouTube, and credible Reddit presence. Expert citations and digital PR — editorial coverage and expert authorship that move a brand from "advertised a lot" to "trusted by experts" inside an AI's consensus layer; this is earned, not bought. Structured data everywhere — FAQ, product, review, and how-to schema on every hero page. And prompt-tracking as a KPI — measure how often, and how favourably, the brand appears across ChatGPT, Perplexity, Gemini, Claude, and AI Overviews for a defined prompt set, the AI-era analogue of rank tracking.

The urgency is real and time-boxed. The brands an AI names in 2026 will be hard to dislodge in 2027, because citation patterns compound. The window to claim ingredient and concern authority is open now and narrows as competitors wake up to it.

The roadmap and the verdict

A 12-month sequence.

| Phase | Initiatives | Expected impact | Difficulty | Priority | Dependencies |

|---|---|---|---|---|---|

| Months 1 to 3 | Lock brand impression share, sister-brand and reseller exclusion governance, PMax brand-exclusion and asset-group rebuild, schema and FAQ on hero PDPs, feed re-titling, baseline prompt-tracking | Efficiency recovery, AI-readiness baseline, no more self-cannibalisation | Low to Medium | Highest | Analytics, Merchant Center, dev for schema |

| Months 4 to 6 | Non-brand category and concern search expansion, ingredient content hubs (first 5 to 8), review-acquisition engine, UGC and creator pipeline, retail-media build (Amazon, Flipkart, quick-comm) | Incremental new-customer acquisition, first AI-citation gains, purchase captured where it happens | Medium | High | Content team, creator ops, retail-media setup |

| Months 7 to 9 | YouTube concern-education at scale, comparison and "best for" content, subscription and replenishment migration to owned channels, digital PR and expert authorship | Lower blended CAC, rising AI shortlist inclusion, LTV improvement | Medium to High | High | Editorial and PR capacity, CRM and WhatsApp infrastructure |

| Months 10 to 12 | Full-funnel measurement (incremental ROAS), entity and knowledge-graph consolidation, advanced retention and win-back, conquest scaling against weak external rivals | Compounding efficiency, defensible AI-search position, share gains | High | Medium to High | Clean measurement model, mature content corpus |

The sequencing logic: fix the leaks and build the machine-readable foundation first, then expand acquisition and start the citation flywheel, then shift growth onto cheaper owned and earned channels, then consolidate the moat.

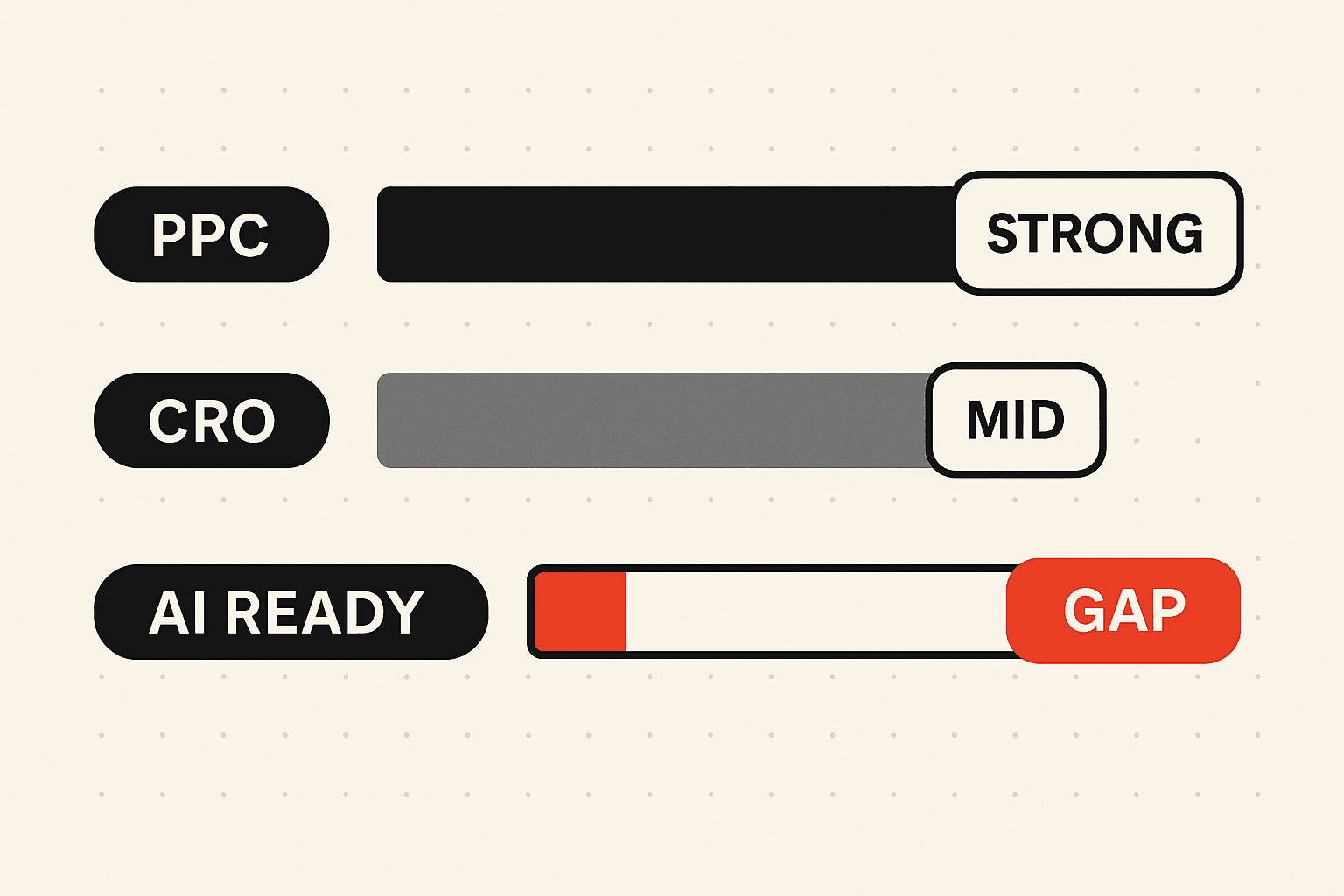

The verdict.

Strong raw ingredients — brand, hero SKUs, demand — but no visible deliberate AEO or GEO programme. AI-search readiness is the single biggest unguarded flank.

What Mamaearth is likely doing well: brand-demand creation at a scale almost no Indian D2C peer can match; hero-product discipline, with a small number of named, ingredient-led SKUs doing the heavy lifting; a genuine strategic pivot away from raw performance spend toward brand-building and media-mix discipline, visible in the FY26 recovery and margin expansion; and a House of Brands that functions as a compounding launch platform, not a single product line.

What Mamaearth is likely missing: a deliberate answer-engine strategy on exactly the ingredient and concern queries its products are built for; sufficient non-brand and concern-led search and content depth, leaving it paying to harvest demand it already created; retention and subscription economics strong enough to take replenishment off cold paid; and full weight behind retail media and quick commerce, where the purchase increasingly happens.

The biggest growth opportunities: own the ingredient and concern answer layer before competitors and before AI citation patterns harden; migrate replenishment to owned channels to structurally lift blended return on ad spend; and premiumise selectively (the Lumineve and serum direction) to enter the faster-growing tier without abandoning the mass-premium base. The most dangerous threats: AI disintermediation of branded and ingredient discovery; strategically owned rivals with deep pockets; and the tier-growth mismatch.

| Dimension | Score (out of 10) | Reasoning |

|---|---|---|

| PPC maturity | 7.5 | Well-funded and sophisticated, but the surface mix lags the discovery shift |

| CRO maturity | 6.5 | Strong trust and mobile UX, thinner on structured proof, bundles, and machine-readability |

| AI-search readiness | 4.5 | Strong raw ingredients (brand, hero SKUs, demand) but no visible deliberate AEO or GEO programme |

Mamaearth has already won the expensive battle: it built durable brand demand in a crowded category. The next battle is cheaper to fight but easier to lose by ignoring it. As discovery migrates from feeds and links to AI answers, the brands that win will be the ones an engine can identify, trust, and name inside a five-item shortlist. Mamaearth has the raw materials to be that brand for onion, ubtan, vitamin C, rice, and the concerns they solve. The single highest-return move is to convert its existing advertising-built equity into machine-readable, review-dense, expert-cited authority on its hero ingredients and concerns, while shifting paid budget steadily toward capture (Shopping, retail media), retention, and AI-search readiness, and away from re-announcing itself to cold audiences at rising CPMs. Defend the demand you paid to build. Then go and own the answer.

If you want this lens turned on your own brand, that is the work we do: a forensic SEO and AI-search audit, an AI SEO programme to build answer-engine authority, and the paid-media discipline to capture and retain the demand. Talk to us about a teardown of your own funnel →

Appendices: the supporting analysis

Appendix A — SWOT. Strengths and weaknesses are internal to the brand, opportunities and threats are external.

Strengths. Category-defining brand equity, top-of-mind in toxin-free, ingredient-led personal care with founder-led trust competitors cannot easily replicate. Hero-SKU economics, with a focused set of named products (Onion Shampoo, Ubtan and Rice face wash, Vitamin C range, Rosemary anti-hair-fall) doing the heavy lifting, Rice Face Wash reportedly reaching a Rs 100 crore ARR run rate. Scale and capital, the parent deploying Rs 788 crore on advertising in FY26 and turning a Rs 200 crore profit with its first-ever dividend declared. A House of Brands flywheel, with The Derma Co (above Rs 750 crore ARR, India's number one sunscreen by Euromonitor) proving the parent can incubate new winners faster each cycle. And omnichannel reach across own D2C, Amazon, Flipkart, Nykaa, and an offline footprint of 2.5 lakh-plus outlets and rising.

Weaknesses. Brand-search dependency, with the keyword profile skewing heavily branded, implying under-developed non-brand category capture. Thin structured proof for the AI era, with limited visible schema, clinical framing, and machine-readable evidence on hero pages. Retention under-leverage, with replenishment appearing to lean on paid re-acquisition rather than owned-channel and subscription loops. A tier ceiling, with the core sitting in the mass-premium (Rs 200 to 500) band, the slower-growing tier. And leadership churn, with a recent CMO transition introducing strategic-continuity risk.

Opportunities. Answer-engine authority on ingredient and concern queries, an open and time-boxed window. Retail media and quick commerce growth, capturing purchase intent where it now concentrates. Selective premiumisation into the faster-growing mid-premium tier via serums, actives, and the Lumineve direction. And conquest of weakening rivals such as WOW Skin Science and overlapping naturals like Biotique.

Threats. AI disintermediation of branded and ingredient discovery. Strategically owned competitors with deep capital: HUL behind Minimalist, Nykaa behind Dot and Key, KOSE behind Foxtale, L'Oreal and Galderma fielding CeraVe and Cetaphil. Rising CPMs and signal loss degrading paid efficiency across the category. And margin pressure if growth continues to require high advertising intensity.

Appendix B — Market structure and positioning. The Indian skincare and BPC market is best understood as a set of price tiers with very different growth rates. This is the structural backdrop to every recommendation here.

| Tier | Price band | Approx. market share | Growth (CAGR) | Representative brands | Mamaearth's relationship |

|---|---|---|---|---|---|

| Mass | Under Rs 200 | ~40 percent | Low | Pond's, Nivea, Himalaya, Lakme, Garnier | Below Mamaearth's core |

| Mass-premium | Rs 200 to 500 | ~25 percent | ~9 percent | Mamaearth, The Derma Co, WOW, Biotique | Mamaearth's core tier |

| Mid-premium | Rs 500 to 1,500 | ~20 percent | ~18 percent (fastest) | Minimalist, Dot and Key, Plum, Foxtale, Pilgrim, mCaffeine | Mamaearth under-indexed here |

| Premium and prestige | Above Rs 1,500 | Smaller, growing | Healthy | Forest Essentials, Kama Ayurveda, global prestige | Honasa entering via Lumineve |

The positioning thesis: Mamaearth's centre of gravity sits in the tier with the slowest growth. That is not a crisis, because mass-premium is also the largest D2C-addressable tier and Mamaearth leads parts of it. But it does mean the brand's future growth ceiling depends on two moves: defending and consolidating mass-premium leadership through superior discovery, including AI search, and laddering selected buyers up into the mid-premium and prestige tiers through actives, serums, and the parent's premium launches. The content and AI-visibility recommendations serve both moves at once, because ingredient-led authority is exactly what pulls a mass-premium buyer toward a higher-consideration purchase.

Appendix C — Advertising-intensity benchmark. Because the only hard channel figure available is total ad spend, it is worth framing what that number means relative to peers.

| Metric | Mamaearth / Honasa | D2C beauty norm | Read |

|---|---|---|---|

| Ad spend as percent of revenue (FY26) | ~33 percent (Rs 788 cr on Rs 2,392 cr) | 40 to 50 percent | Lower intensity than peers, and falling deliberately |

| FY24 comparison | ~34.6 percent (Rs 664 cr on Rs 1,920 cr) | n/a | Consistent, slightly declining intensity |

| Direction of travel | Toward brand-building and efficiency | n/a | The pivot is real and stated by management |

The popular narrative that Mamaearth simply out-spends everyone is only half right. It spends a great deal in absolute terms, but proportionally less than the typical D2C beauty challenger, and it is actively reducing that proportion while still growing. The strategic risk is not that the brand spends too much. It is that a meaningful share of that spend may be pointed at channels and surfaces the discovery shift is eroding. Re-pointing spend, not cutting it, is the thesis.

Appendix D — AI-search risk and opportunity register. A concrete, prompt-level register of where the brand is most exposed and most able to win in answer engines. These are example buyer prompts any operator can run today to test their own visibility.

| Example buyer prompt | Engine likely consulted | Risk to Mamaearth | Opportunity to win | Priority |

|---|---|---|---|---|

| "best onion shampoo for hair fall in India" | ChatGPT, Google AI Overviews | Medium (rivals copy the angle) | High (brand owns the onion association) | Highest |

| "best face wash for oily skin under 400" | ChatGPT, Perplexity | High (price tier crowded) | High (Ubtan, Vitamin C fit) | Highest |

| "is salicylic acid or niacinamide better for acne" | Perplexity, Gemini | High (loses to clinical brands) | Medium (needs ingredient hub) | High |

| "Mamaearth vs Minimalist vitamin C" | ChatGPT, Google | Medium (owned by whoever writes the comparison) | High (own the comparison page) | High |

| "dermatologist recommended sunscreen India" | All engines | High (CeraVe, Cetaphil advantage) | Low to Medium for the Mamaearth brand | Medium |

| "safe baby lotion for newborns" | ChatGPT, Google | Low (brand trust is strong) | High (defend and extend) | High |

| "best vitamin C serum for sensitive skin" | ChatGPT, Perplexity | High | Medium | High |

| "natural shampoo without sulphates" | Gemini, Google | Medium | High (natural positioning) | High |

The highest-priority rows are where buyer language overlaps perfectly with a Mamaearth hero ingredient and a winnable price point. Those are the prompts to instrument in prompt-tracking first, to build ingredient-hub and review density around first, and to measure relentlessly. The "dermatologist recommended" rows are where the brand should flank rather than fight, leaning on natural-plus-tested rather than contesting pure clinical authority head-on.

Appendix E — KPI and measurement framework. A mature programme needs metrics for both the classic auction world and the emerging answer-engine world. The second column is the part most brands have not yet built.

| Layer | Classic KPI | AI-era KPI |

|---|---|---|

| Visibility | Impression share, organic rank | Prompt-set citation rate across ChatGPT, Perplexity, Gemini, Claude, AI Overviews |

| Acquisition | CAC, ROAS, conversion rate | AI-referred traffic share and its conversion premium |

| Demand quality | Brand vs non-brand split | Share of voice on solution-aware and ingredient prompts |

| Efficiency | Blended ROAS | Owned-channel revenue share (paid-independence ratio) |

| Retention | Repeat rate, LTV | Subscription penetration, replenishment-on-owned share |

| Content | Rankings, sessions | Citation density on review and editorial surfaces (Reddit, YouTube, press) |

What gets measured gets defended. Today almost every D2C dashboard measures the auction and ignores the answer. Standing up prompt-tracking and an owned-channel-share metric is, by itself, a competitive advantage, because it lets a brand see the discovery shift happening in time to act on it rather than after a quarter of unexplained ROAS decline.

Appendix F — Prioritisation model (impact vs effort). A consolidated ICE-style ranking of the recommendations, so the programme can be sequenced by return rather than by enthusiasm. Each initiative is scored 1 to 10 on Impact (revenue or efficiency upside), Confidence (how sure the play is to work), and Ease (inverse of effort and cost). The ICE score is the average, meant for relative sequencing rather than forecasting.

| Initiative | Impact | Confidence | Ease | ICE | Tier |

|---|---|---|---|---|---|

| Brand impression-share defence and reseller and sister-brand exclusions | 8 | 9 | 9 | 8.7 | Do first |

| Schema and FAQ on hero PDPs (machine-readability) | 8 | 8 | 8 | 8.0 | Do first |

| PMax brand-exclusion and asset-group rebuild | 8 | 8 | 7 | 7.7 | Do first |

| Shopping and PMax feed re-titling (ingredient plus concern) | 7 | 8 | 8 | 7.7 | Do first |

| Prompt-tracking baseline across AI engines | 7 | 7 | 8 | 7.3 | Do first |

| Ingredient content hubs (hero ingredients and concerns) | 9 | 8 | 5 | 7.3 | Build next |

| Review-acquisition engine on AI-cited surfaces | 9 | 7 | 5 | 7.0 | Build next |

| Non-brand category and concern search expansion | 8 | 7 | 6 | 7.0 | Build next |

| Retail media and quick-commerce build | 8 | 7 | 6 | 7.0 | Build next |

| Subscription and replenishment migration to owned channels | 9 | 7 | 4 | 6.7 | Build next |

| Comparison and "best for" content (conquest plus AI) | 7 | 7 | 6 | 6.7 | Build next |

| YouTube concern-education at scale | 7 | 6 | 6 | 6.3 | Scale later |

| Digital PR and expert authorship | 8 | 6 | 4 | 6.0 | Scale later |

| Entity and knowledge-graph consolidation | 8 | 6 | 4 | 6.0 | Scale later |

| Full-funnel incremental-ROAS measurement | 7 | 6 | 5 | 6.0 | Scale later |

| Conquest scaling against weak external rivals | 6 | 6 | 6 | 6.0 | Scale later |

The "do first" tier is almost entirely cheap, fast, and high-confidence. It stops the leaks (self-cannibalisation, brand-demand harvesting misreported as prospecting) and lays the machine-readable foundation everything else builds on. The "build next" tier is where the durable advantage is created, and it is deliberately harder, because content depth, review density, and retention loops take time and cannot be bought overnight. The "scale later" tier compounds the moat once the foundation and the flywheel exist. A common and expensive mistake is to start with the glamorous "scale later" work before the foundation is in place, which wastes spend on surfaces a brand is not yet equipped to convert or measure.

Disclaimer: This study is based on publicly available information, observable advertising activity, third-party intelligence tools, and strategic inference. Hard figures are drawn from company filings, earnings commentary, and named industry sources. Where the company does not disclose a number, the analysis uses directional estimates and benchmark ranges, which are identified as such in the text. No claim is made that the authors have worked with, or had access to internal data from, Mamaearth or Honasa Consumer Limited.

Aditya Kathotia

Founder & CEO

CEO of Nico Digital and founder of Digital Polo, Aditya Kathotia is a trailblazer in digital marketing. He's powered 500+ brands through transformative strategies, enabling clients worldwide to grow revenue exponentially. Aditya's work has been featured on Entrepreneur, Economic Times, Hubspot, Business.com, Clutch, and more. Join Aditya Kathotia's orbit on LinkedIn to gain exclusive access to his treasure trove of niche-specific marketing secrets and insights.